Last week, quite a few of my friends in Gowanus received letters from the Federal Emergency Management Agency (FEMA) regarding updated flood maps for New York City.

The Agency encourages everyone to identify their property's flood risk by checking the Preliminary Flood Insurance Rate Maps.

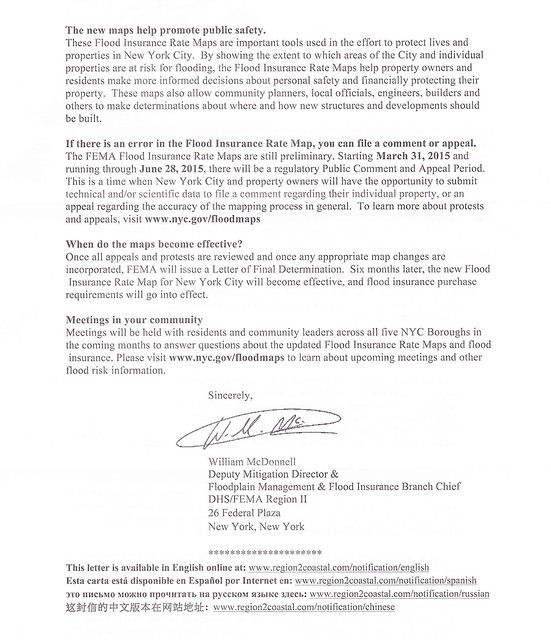

In the letter, FEMa stresses that the maps are only preliminary. A public comment and appeal period began on March 31st, 2015 and will continue until June 28th, 2015. During this period, homeowners can challenge FEMA's new maps by sending technical and/or scientific data regarding their individual property.

After FEMA evaluates all challenges and appeals, the new maps will be incorporated and "flood insurance purchase requirements will go into effect."

What exactly will all this mean for residents in the footprint of the new flood hazard areas?

A Gowanus property owner just reached out to me late last week and sent me some questions that she has forwarded to our public officials regarding this matter:

Where can people find information on how to challenge the proposed maps? Are there any resources available to help people understand the challenge process?

Challenging this designation would require a surveyor or engineer. Are there any resources to help a homeowner with this?

Since people have just received notice of the proposed map changes they have lost at least two weeks of a 90 day comment period. Can this be extended?

Are condominiums and cooperatives treated differently or the same for insurance purposes.

Is there a difference between Zone X and "shaded" Zone X and if so what is it?

Is there some information available about flood insurance affordability?

When can lenders require flood insurance in Zone X?

Obviously, there is quite a bit of uncertainly regarding this matter. Below are just some links that may help.

Here are the flood maps from the FEMA site:

http://floodmaps.fema.gov/prelim/PrelimData/New%20York/Kings%20County/prelim_issue_date-2013-12-05/FIRM/3604970211G.pdf

Here is another site which is a bit easier to use:

http://www.region2coastal.com/view-flood-maps-data/what-is-my-bfe-address-lookup-tool/

For background and information on how to object to the proposed flood maps here is the link to the notice that was published in the Federal Register:

https://www.federalregister.gov/articles/2015/03/16/2015-05852/proposed-flood-hazard-determinations#h-4

.JPG)

8 comments:

Yep received one of these and I live in Columbia Waterfront. What this letter doesn't tell you is that flood insurance is underwritten by the Feds and in subterranean rooms the ONLY thing it will cover are items like a washer and dyer. So if you live in a basement apartment and got this letter, yes your are at risk of flooding but the vast majority of your home interiors will NOT be covered. So weigh up the options/risk of living there and/or getting flood insurance.

This is a very helpful NYC flood insurance site:

http://floodhelpny.org/

Re X zones,:

Shaded Zone X are areas that have a 0.2% probability of flooding every year (also known as the "500-year floodplain"). Properties in Shaded Zone X are considered to be at moderate risk of flooding under the National Flood Insurance Program. Flood insurance is not required for properties in Zone X. Local floodplain zoning ordinances do not apply to Zone X.

Unshaded Zone X are areas that are above the 0.2% flood elevation. Properties in unshaded Zone X are considered to be at low risk of flooding under the National Flood Insurance Program. Flood insurance is not required for properties in Zone X. Local floodplain zoning ordinances do not apply to Zone X.

Many who got the letter don't get to weigh the risks, but are mandated to purchase the flood insurance. As the letter points out, if there is a federally backed mortgage on the building in Zone A, or there was FEMA money used to rebuild (under the Build-it-Back Sandy Program) you are obligated to purchase the insurance.

And as was explained at the FEMA presentation on this, in Red Hook, your insurance will be less if you get into the program now--that insurance levels have been mandated by congress to go quite high.

Anyone with a mortgage on a building in Zone A might want to pay attention to this now.

Great info. Thanks Shanone, Andrea and Anon.

The site is good at showing the FEMA data, limited solely to the transition, but lacks several things:

- What's the date of the Preliminary maps? there was a release in 2013 and another one in 2015...yeah confusing

- What if my property is crossed by multiple zones? is the declared zone the result of a latitude and longitude check or a property (structure) check?

- what about the future? climate change, sea level rise are supposed to affect floodplains even as close as 2020. If you truly want to plan, you need to consider it.

- How can I contest the map? Yes, I'm not an expert, but I don't know what the amount of error and uncertainty exists in these maps so it is likely limitations and mistakes were done.

I can't imagine this will have a positive effect for property values.

There are discrepancies between the websites. Floodnyc may indicate a zone is not changing where the Region2coastal site has that same property in an AE zone. Triple check the various maps especially if you own property on Bond Street.

The comment period is over at the end of June so we need our questions addressed now especially is people are going to appeal.

I called the FEMA number on the back of the letter to try to get some information/clarification on the appeal process. I mentioned the delayed notice and asked whether FEMA would be scheduling more meetings. I was referred to the map administrator at DOB and the person I spoke with was doing their best to be helpful but DOB isn't the right party for the questions I had and said I should contact FEMA again.

Post a Comment