Gowanus Canal overflowing its banks during Hurricane

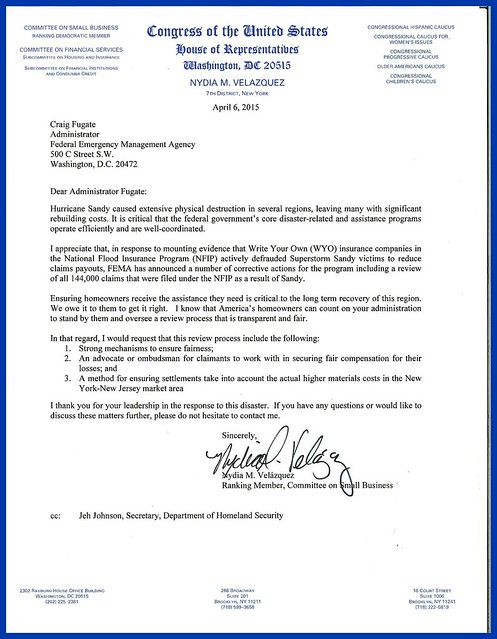

Congresswoman Nydia Velázquez’s letter to the FEMA Administrator regarding

the National Flood Insurance Program and its process for reopening claims.

In the past few days, the Federal Emergency Management Agency (FEMA) sent out letters regarding updated flood maps for New York City to all property owners in or near the Special Flood Hazardous Area newly identified by the federal agency.

The Agency encourages everyone to identify their property's flood risk by checking the Preliminary Flood Insurance Rate Maps. The maps can be accessed here and here.

In the letter, FEMA stresses that the maps are only preliminary. A public comment and appeal period began on March 31st, 2015 and will continue until June 28th, 2015. During this period, homeowners can challenge FEMA's new maps by sending technical and/or scientific data regarding their individual property.

After FEMA evaluates all challenges and appeals, the new maps will be incorporated and flood insurance purchase requirements will go into effect.

Above also please fine Congresswoman Nydia Velázquez’s letter to the FEMA Administrator Craig Fugate regarding the National Flood Insurance Program and its process for reopening claims.

Her office has been very helpful in this matter.

A few days ago, I was contacted by Antony Gemmell, Staff Attorney for New York Legal Assistance Group, a non-profit organization which provides free legal services to people who were impacted by Superstorm Sandy.

Gemmell let me know that New York Legal Assistance Group "offers advice and representation on a wide range of legal issues related to Sandy, including flood insurance."

Please avail yourself of the organization's services by contacting NYLAG's Storm Response Unit (SRU) client intake team at (212) 584-3365 or stormhelp@nylag.org.

If you received the FEMA letter because your property is either is zone A or Zone X, you need to take the time to understand what all of this will mean. This has some very important ramifications beyond getting flood insurance.

The Agency encourages everyone to identify their property's flood risk by checking the Preliminary Flood Insurance Rate Maps. The maps can be accessed here and here.

In the letter, FEMA stresses that the maps are only preliminary. A public comment and appeal period began on March 31st, 2015 and will continue until June 28th, 2015. During this period, homeowners can challenge FEMA's new maps by sending technical and/or scientific data regarding their individual property.

After FEMA evaluates all challenges and appeals, the new maps will be incorporated and flood insurance purchase requirements will go into effect.

Clearly, this is an important issue for homeowners in both Gowanus and Red Hook. The information created by FEMA has generated more questions and has left many owners confused, as they are trying to navigate through this process in a relatively short time period.

FEMA has held a community meeting in Red Hook two weeks ago. After residents called for a similar meeting in Gowanus, FEMA and the City have just announced that they will be happy to organize an informational meeting in the Gowanus/ Carroll Gardens area.

That is good news. I will be posting information on the meeting as soon as a date has been set, so stay tuned.

Her office has been very helpful in this matter.

A few days ago, I was contacted by Antony Gemmell, Staff Attorney for New York Legal Assistance Group, a non-profit organization which provides free legal services to people who were impacted by Superstorm Sandy.

Gemmell let me know that New York Legal Assistance Group "offers advice and representation on a wide range of legal issues related to Sandy, including flood insurance."

Please avail yourself of the organization's services by contacting NYLAG's Storm Response Unit (SRU) client intake team at (212) 584-3365 or stormhelp@nylag.org.

If you received the FEMA letter because your property is either is zone A or Zone X, you need to take the time to understand what all of this will mean. This has some very important ramifications beyond getting flood insurance.

.JPG)

10 comments:

Another day, another question or five.

I'm encouraged that there will be another meeting for Gowanus/Carroll Gardens property owners. CWD property owners also shouldn't be forgotten.

If we should try to do our best to make sure our our neighbors are aware of these potential changes especially if they are not big users of social media or the Internet. Let them know about the NY Legal Assistance Group.

FEMA operating manual:

1. Be unprepared to respond to actual emergencies.

2. Terrorize and Obfuscate with bureaucracy.

3. Back to 1.

If people are able to speak with an attorney from NYLAG or elsewhere one of advantages is that they will explain things clearly and not obfuscate with bureaucracy or politispeak.

"This has some very important ramifications beyond getting flood insurance."

Like what?

Like having to sacrifice the ground floor of your building. For many that means giving up rental income. It also means losing 1/3 or 1/4 of your homes value if you can't use the ground floor.

Like being forced to sell your home or losing it to foreclosure because of the high cost of flood insurance. If you have a mortgage and are now required to buy flood insurance and do not the bank will purchase it for you. Maybe there are some programs for senior citizens or those with moderate incomes. If so, maybe FEMA and the local electeds can engage in some outreach.

Being in a flood zone could lower property values and that could cause a ripple effect.

I got a letter, but I'm not in either zone (though I am close to X). So the distribution was a bit wider than just those in the zones (so everyone knows.)

Katia, did you get a letter? I'm around the corner from you, and I didn't, but I think we're just outside the zone. Am I correct?

No, I did not get a letter. I am not in the flood zone according to the FEMA maps.

In some condo/coop developments that are comprised of separate building with separate addresses there can be a range of zones from none to A so would Zone A apply to all buildings in the development? And would coop or condo owners also be required to purchase their own flood insurance even if they are on the 12th floor?

Post a Comment